Car insurance rates for teenage driver differ significantly from those of experienced drivers. Your teenager has probably been waiting for their driver’s license from the moment they turned 16. If you’re thinking about letting your teenager drive your car, or if you’re going to buy them their own vehicle, you need to take insurance into account right away.

Can I drive my parents’ car without being on the insurance?

Auto insurance is a contract between drivers and an insurance company. The policy typically covers property damage, theft, and medical bills. While auto insurance generally follows the vehicle rather than the individual driver, teenagers living under their parents’ roof must be explicitly listed on their parents’ auto insurance policy.

If a teenager gets into a car accident and is not legally listed on the policy, the insurance company can deny the claim entirely. Furthermore, Ontario insurance companies strictly require the addition of a secondary driver if that person will be operating the vehicle on a regular basis. It is best practice to add a teenager to an insurance policy as soon as they receive their G2 license.

In Ontario, if you are driving without proper coverage or fail to disclose household drivers, you risk receiving heavy fines, severe penalties, and drastically increased insurance rates. You may also be labeled a high-risk driver, or have your license suspended. It is simply not worth the risk.

How much is car insurance for a new teenage driver in Ontario?

Parents sometimes hesitate to add teenagers to their auto insurance because new drivers lack experience and are considered higher risk by insurance providers. However, ensuring they are properly covered is vital to protecting your family’s financial future.

When calculating premiums, insurance companies evaluate the driver’s abstract (whether they have received tickets or been in a crash), their geographic location, and the type of car being driven. While the average yearly cost for an experienced driver in Ontario falls between $1,300 – $1,800, a brand-new driver can generally expect to see premium rates ranging from $3,200 to $7,200 if insuring their own vehicle. Adding them as a secondary driver to an existing family policy is almost always the more affordable route.

Crucial 2026 Update: Protecting your teenage driver on the road

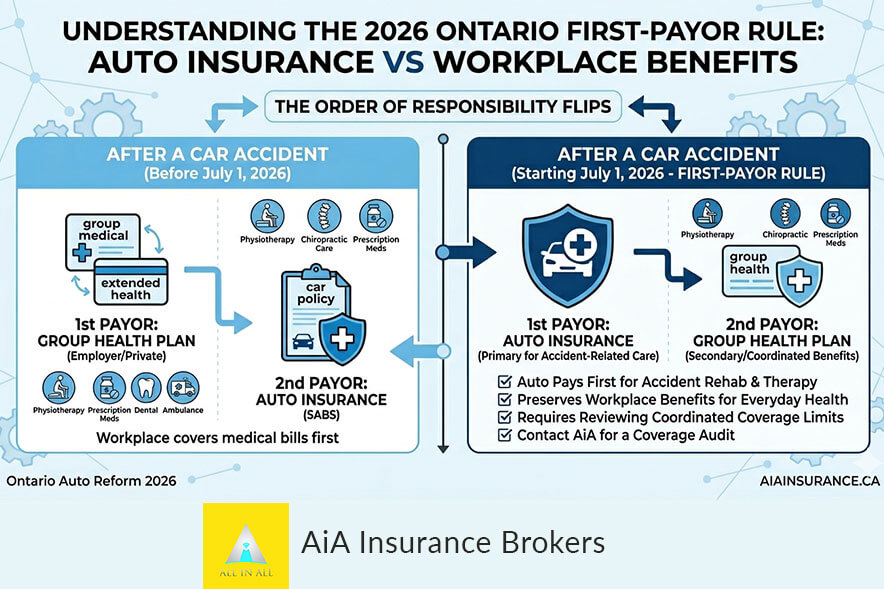

Ontario’s recent landmark auto insurance reforms completely changed how injuries and financial recovery are handled after an accident. This makes listing your teenage driver more critical than ever before.

Previously, standard auto policies automatically included a blanket set of Statutory Accident Benefits (SABS) to protect everyone in the household. .Under the current rules established by the Financial Services Regulatory Authority of Ontario (FSRA), only basic medical and rehabilitation care remain mandatory. As detailed by the Insurance Bureau of Canada, vital financial protections that directly impact young people—such as Lost Educational Expenses and the Non-Earner Benefit—have become completely optional

Lost Educational Expenses: If a serious car accident prevents your teenager from attending school, their lost tuition, textbooks, and semester expenses are no longer covered by default. Parents must explicitly opt into this coverage.

Non-Earner Benefits: Because most teenagers are full-time students or only work part-time, they do not qualify for standard income replacement. Instead, they rely on the “Non-Earner” benefit if an injury severely disrupts their daily life. This is also now an optional add-on.

Because these optional family protections strictly apply only to named insureds and explicitly listed dependants, failing to add your teenager as a declared driver on your policy could leave them completely unprotected from these severe financial gaps.

How do you add a teenage driver to an Auto Insurance Policy?

If a parent shares a vehicle with a teenage driver, the teen will be listed as a secondary (or occasional) driver. A secondary driver is someone who operates the vehicle frequently but does not drive it as often as the primary user.

While adding a teenager to your insurance will cause your premium rate to increase (often by roughly 44%), it is vastly cheaper than buying them an individual policy. If you are ready to add your teen, simply contact your insurance broker to update your household driver list and review your accident benefit options. If you want to explore more budget-friendly paths, you can also look into modern telematics programs (Safe Driver Apps), which track driving habits like smooth braking and award major discounts to safe young drivers without cutting back on essential coverages.

Parents should speak openly with their teenagers to ensure they understand the mechanics of an auto policy and the serious real-world repercussions of a collision. Practicing safe, defensive driving is the absolute best way to protect your family and keep your insurance rates from rising.

If you’re looking to switch insurance companies, get quotes from various companies to see which one will offer you a price within your budget. Parents should speak to their teenagers to ensure they have an understanding of what an auto insurance policy is and what the repercussions will be if they end up in an accident. Safe and defensive driving is the best way to prevent insurance rates from rising.

AiA Insurance offers fair auto insurance rates. We make auto insurance plans tailored to your needs. Having auto insurance protects you and your family after an accident. Get in touch with us today for a quote.